Summary

Fully-Paid Securities Lending (FPL) lets you lend fully owned stocks or ETFs to potentially earn additional passive income, depending on market demand. You remain the owner, can sell at any time, and still receive dividends and distributions. Learn how the lending process works and the key risks to keep in mind.

What is Fully-Paid Securities Lending?

At its core, Fully-Paid Securities Lending (FPL) allows investors who own their shares outright to lend those shares to the market in exchange for a lending fee.

Securities lending is not a disposition (selling) of your securities. You still see the position in your account and can place an order to sell at any time.

You’re simply letting your long-term holdings do a bit of extra work in the background.

For investors accustomed to two traditional return streams - dividends and price appreciation from stocks and Exchange Traded Funds – securities lending introduces a third potential source: lending revenue. It isn’t guaranteed, but when demand aligns with what you own and your securities are lent, it can add incremental, passive income to your portfolio.

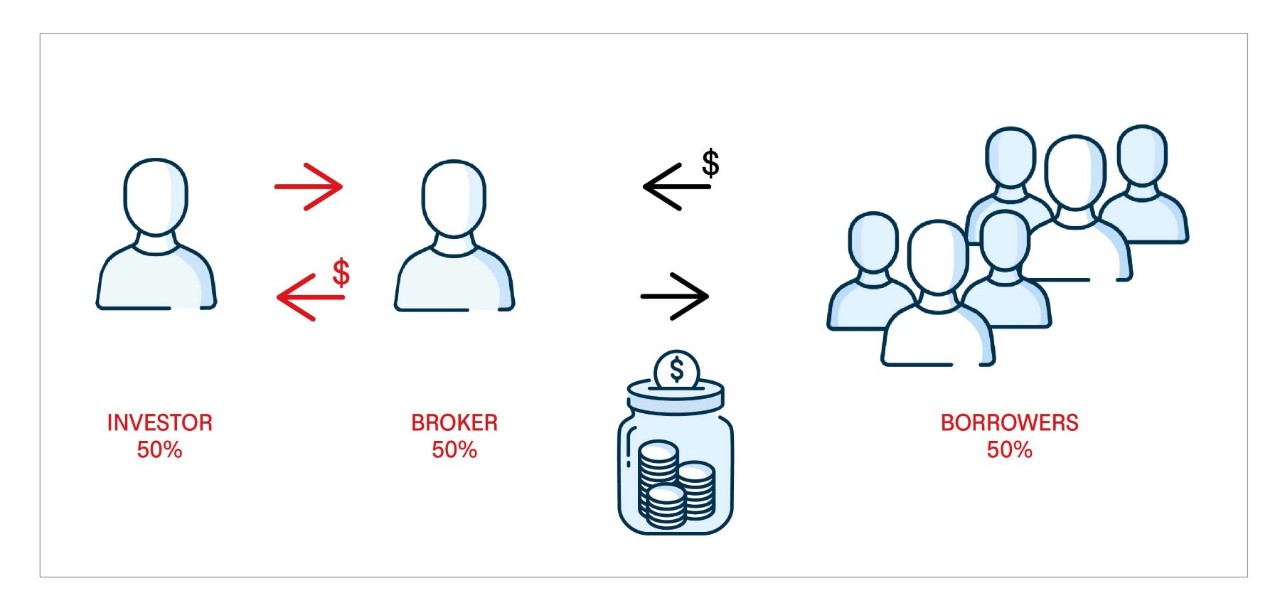

How does securities lending work?

Once an investor has enroled their account(s) for securities lending, the eligible securities (stocks and ETFs) become available for lending. The investor deals with their broker and when a potential borrower needs a security the broker will match it and deliver the securities to the borrower. While this occurs high quality collateral is set aside as a cushion- typically 105% of the securities value, marked to market daily. The borrower pays the broker a lending fee of which 50% is paid to the investor as interest income.

Securities lending process

While your securities are enrolled, there are some points to consider:

- You can sell your securities anytime, even when they are borrowed.

- If your security pays dividends or distributions, you will receive them.

- CND & U.S stocks and ETFs are eligible

- Available in registered and non-registered accounts

- The lending fee is split between the investor and broker

Is securities lending risky?

Fully paid securities lending does carry some risk, although the risk for the investor is considered low. When securities are being borrowed in the case of dealer (broker) insolvency the investor loses the coverage of the Canadian Investor Protection Fund (CIPF). To safeguard investors in the unlikely event of a default, borrowed securities are backed by high quality collateral set aside that provides 105% protection, which is marked to market and reviewed daily.

What are borrowed securities used for?

The market borrows shares for mundane but critical reasons:

- Short selling: Some traders sell shares they don’t currently own, planning to buy them back later. To make good on delivery when they sell short and borrow the shares, often sourced from fully paid lending inventory.

- Settlement logistics: Brokers need to deliver shares to settle client trades on time.

- Market makers borrow securities to create liquidity in the market.

- To build and unwind financial products such as ETFs, mutual funds, and market linked notes.

What Drives the Income?

Demand, plain, and simple. Securities' lending revenue rises and falls with borrower demand for specific names, and that demand can shift quickly. Large capitalization liquid stocks that are widely held (think of Blue chips) - are typically ‘’easy to borrow’’ and have low borrowing fees, often below 1%. By contrast, “hard to borrow” (HTB) names - driven by elevated short interest, special situations, or security specific news can attract meaningfully higher rates with “warm” inventory commonly ranging from about 1% to 10% and truly scarce shares sometimes exceeding 10%.

- Easy to borrow shares can become hard to borrow and vice versa.

- Borrowing rates change frequently, the income earned will fluctuate.

- No guarantees which securities will be in demand or when.

Why Lend Fully Paid Securities?

Fully paid securities lending doesn’t change your market exposure or your underlying investment strategy. You still own the position and can sell at will, with the loan unwound so your trade settles normally. Investors give up nothing by participating in a securities lending program. Instead, it provides an additional source of income on your current assets. From an investor’s perspective, the program is hands-off: the process is automated and when the securities are in demand, they are borrowed and then returned, and you get paid.

With availability across cash, margin, TFSA, and other eligible registered accounts, the route to participation is wider than ever. For many investors, however, the case for securities lending is growing increasingly compelling.

You built your portfolio having in mind your financial objectives. Fully-paid Securities Lending allows you to have additional passive revenue despite price fluctuations, without you having to do anything and is even more accessible now with the addition of registered accounts. Even if the revenue is not guaranteed and can be random, it is revenue that you would not have otherwise and for free!

Interested in this program?

Key takeaways:

- Fully-Paid Securities Lending (FPL) lets investors lend fully owned stocks/ETFs in exchange for a lending fee.

- You remain the owner and can sell at any time; dividends/distributions are still paid to you.

- Income is demand-driven and can fluctuate as borrow rates change (easy-to-borrow vs hard-to-borrow names).

- Investor risk is generally considered low and mitigated by high-quality collateral (marked to market daily), but investor-protection coverage may not apply while the securities are on loan.

- The program is automated and available in registered and non-registered accounts (subject to eligibility).